Introduction

As many readers know, I work in medical sales. When I read the annual letter and 10‑K for HIMS, I related to this company as an operator and would‑be owner more than I do with most businesses I look at. My goal, ever since I was young, has been to own a business. Early on, I was told that if you want to be a businessman, you need to understand sales. Ten years into a sales career, I can confirm that was excellent advice. At the right company, being in sales is effectively like running your own small franchise inside a larger organization.

Sales is, however, brutally competitive—especially on a residual‑based model. That’s why whenever I look at a business, the first thing I evaluate is the moat. The businesses I hate are the ones where customer retention ultimately comes down to which salesperson the staff likes more.

The Pathology Example and Moats

That dynamic is the foundation of many medical sales organizations. Take pathology, for example: once you set up a clinic, you need to move quickly to get them integrated with EMR systems, establish recurring pickups, and connect them with billing teams who can handle frustrated patients. Even all of that is a pretty thin moat.

What is very difficult to dislodge is a ten‑year relationship with a rep. That puts the chips in the representative’s hands and forces the pathology lab either to pay more to keep that rep or risk losing them—and the business—to a competitor lab.

There is a third option, and it’s the smartest one: make the lab so efficient and sticky to the clinic that neither the rep nor the clinic wants to leave. If the clinic feels like switching labs would create chaos, and the rep feels like no other lab can match the support and economics, then the lab finally owns the relationship.

This is a very commonsense way to think about business, but it’s often overlooked. Warren Buffett preaches the importance of a moat, but you don’t have to take it from him. It’s obvious if you’ve ever sold anything and taken the perspective of the owner signing your paycheck.

How HIMS Fits the Distributor Model

HIMS is unusual because it acts as both a distributor and a compounding pharmacy. There are thousands of compounding pharmacies and thousands of medical distributors in the U.S., which means HIMS has to differentiate itself in a crowded field.

The medical industry is built around the distributor model. At a high level, it is usually more attractive for a new product or drug to go through an existing distributor than to build an in‑house sales force. Founders of new therapies typically don’t have the skill set—or the desire—to also be sales leaders. Medical sales is complicated and relationship‑heavy: there are countless clinics, and most of them require an expensive lunch just to let you present. Sometimes even that isn’t enough.

Once you get into enough individual doctors’ offices, you then have to convince those doctors to request your product at the hospital. If you get enough of those requests, you might get approved at the hospital. Very few scientists have the time or temperament to create a new drug and then fight through bureaucracy and an ungodly number of personalities in the field.

So you get a web of distributors, some small and some huge. Maybe the new drug company signs a royalty deal with McKesson or Cardinal Health. Maybe a niche graft company starts locally and tries to cover Illinois with five independent distributors.

Those distributors then create webs of their own. It’s often just some guy or girl who connects a network of people. Say the graft company offers this person 20%, and then that person offers 50% of her cut to the people in her network, who then do the same thing downstream. That chain continues until the margin is so thin it’s no longer worth anyone’s time. Service quality deteriorates, and the model doesn’t scale. These arrangements tend to show up in short‑lived products where everyone wants a quick hit until the product is either commoditized or rolled up into one of the big distributors.

Cardinal Health, McKesson, and Cencora (formerly AmerisourceBergen) dominate U.S. drug distribution. They control more than 90% of the market, generate hundreds of billions in revenue, and live on razor‑thin margins—roughly mid‑single‑digit gross margins and around 1% operating margins. HIMS, on the distribution side of its business, is playing on that same thin‑margin field.

The distribution model can be extremely lucrative for an individual rep with a tight, loyal panel of prescribers. If I have a close‑knit group of 10 productive doctors and enough products to sell them, I can plausibly earn seven figures a year. The moment I try to turn that into a big web where other people do the work for me, the economics start to erode. That’s when I stop liking the business.

The Real Engine: Compounding

HIMS understands that distribution is low margin. The real engine is compounding. They buy raw ingredients for pennies, mix them, and sell finished products for cash prices.

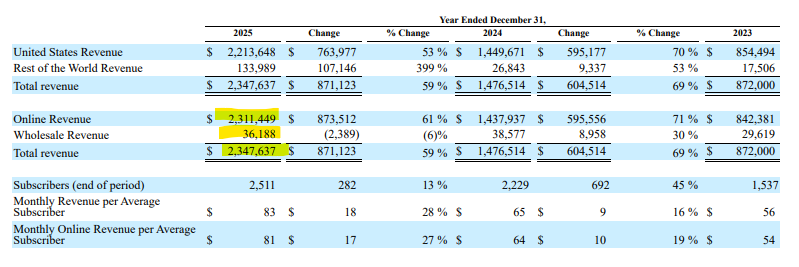

In 2025, HIMS reported about $2.31 billion of online revenue—which is where the compounding and direct‑to‑consumer business sits—and about $36 million of wholesale revenue. Total revenue grew to roughly $2.35 billion in 2025 from $1.48 billion in 2024 and $872 million in 2023.

Management has framed the 2025 weight‑loss GLP‑1 business at around $725 million of revenue. At the same time, gross margin fell from about 79% in 2024 to roughly 74% in 2025. Wholesale revenue ticked down from roughly $39 million to $36 million. Depreciation and amortization jumped from about $17 million in 2024 to about $55 million in 2025 as new compounding facilities came online, and the company incurred higher transportation and cold‑chain costs to ship GLP‑1s.

If you take management’s GLP‑1 revenue target and the change in blended margin, you can back into an implied GLP‑1 gross margin of roughly the high‑50s percent, contributing on the order of $400‑plus million in gross profit. That’s a very healthy margin for a fast‑growing segment.

But the GLP‑1 compounding trade was never going to be a durable business. It was an arbitrage. Under federal law (Section 503A and 503B of the Food, Drug, and Cosmetic Act), pharmacies can only mass‑produce “copycat” versions of a drug when that drug is on the FDA’s official shortage list. By early 2025, the FDA began declaring the semaglutide shortages “resolved.” Once a drug is off the shortage list, it is legally “commercially available,” and mass compounding near‑copies becomes patent infringement, not clever pharmacy work.

2026: The Unraveling

In 2026, the HIMS story broke.

On February 7, 2026, the FDA came down on HIMS for an “illegal copycat” product. HIMS had tried to launch a compounded weight‑loss pill—essentially an oral Wegovy—at $49 for the first month to keep its weight‑loss growth engine humming. Regulators quickly labeled it an illegal copy of a commercially available drug and forced HIMS to pull it within 48 hours.

Two days later, on February 9, Novo Nordisk sued HIMS for mass patent infringement. At that point, the debate about whether HIMS was a telehealth platform or a quasi‑pharmacy ended. In the eyes of Novo and regulators, it looked like an unlicensed drug manufacturer.

The stock then hit what technicians call a “death cross,” with the 50‑day moving average falling below the 200‑day. Short interest spiked well north of 30%. Shares fell more than 70% from their highs.

The Novo Nordisk Deal and the Rebound

Fast‑forward to the recent rally. HIMS shares jumped about 50% on news that Novo Nordisk would distribute Wegovy and Ozempic—including the oral Wegovy pill—through the HIMS platform. In exchange, Novo agreed to drop its lawsuit, and HIMS agreed to stop promoting compounded GLP‑1s.

The primary thing this deal accomplished was to remove the existential legal overhang. Bankruptcy risk from a massive settlement moved off the table. That alone justifies some multiple expansion.

The Street quickly rebuilt a growth narrative. If HIMS can offer the oral pill, it can expand its weight‑loss funnel, because many patients prefer a pill over injections. A second bull argument emerged that weight loss could become a huge top‑of‑funnel product. If HIMS can use GLP‑1 demand to bring a lot of people onto the platform, maybe it can cross‑sell them higher‑margin compounded products for hair loss, sexual health, dermatology, and so on. In other words, GLP‑1s might become the loss leader that drives a more profitable bundle.

On paper, that’s a nice story. I just don’t buy it.