Williams‑Sonoma: Data and Design

Atypical ROIC in Furniture Retailing

Every investor should have a short list of high‑quality stocks in their bag that they’ve studied extensively. The reasoning is twofold.

First, it trains your eye for greatness. Working through a handful of truly exceptional businesses gives you a mental database of what “good” actually looks like – high returns on capital, durable moats, rational capital allocation, clean incentives, and honest, boring footnotes. That pattern recognition is what keeps you away from the kind of businesses that, as Kevin O’Leary likes to say, should be taken out back and shot. Once you’ve internalized what a great business feels like, the pretenders start to smell wrong very quickly.

Second, it prepares you for the hunt. The time to decide what you want to own is before the market is down 25% and CNBC is running recession countdown clocks. In real drawdowns you don’t get calm, leisurely stock screens – you get a firehose of opportunity and a very narrow bandwidth for decision‑making. If you already have a vetted hit list, you’re in position to act. If you’re scrambling to figure out what to buy in the middle of the panic, you’re already behind.

Williams‑Sonoma is one of the names on my own buy list, and it’s a useful case study in the kind of business you want to have pre‑underwritten before the next real drawdown hits. It’s not just about crashes, either. Even in long bull markets, great businesses routinely sell off 10–20% on nothing more than a messy quarter, a short‑term macro scare, or a sector rotation. If you’ve already done the work, those “small” dislocations can be great opportunities.

Why Williams‑Sonoma made my list

The first reason I chose to write about Williams‑Sonoma (WSM) is that the stock has been very good to me. I first discovered it in late September 2023 through Joel Greenblatt’s Magic Formula screener. At the time, the company’s market cap sat around $9–10 billion, net income was tracking toward roughly $1.1 billion (where it ultimately landed), and free cash flow, excluding stock‑based comp, was around $1 billion.

The return metrics were very attractive. Over the prior decade, WSM’s ROIC and ROE were exceptional – north of 20% in the early 2010s and ramping toward a consistent 40% in the latter half of the decade. The final push came from closer to home: earlier that year, my wife had spent a small fortune on a Pottery Barn crib and dresser for our first child. My thesis didn’t require much more mental gymnastics. If you can’t beat them, join them. Rather than spend the rest of my life getting gouged by Pottery Barn, I figured I’d buy shares and earn a lifetime rebate. I bought in around $70 a share, and since then, the stock has nearly tripled, most of that gain coming in the first year.

The second reason for revisiting WSM now is to learn more about the housing market from a bottom‑up perspective. Stronger housing demand tends to lift a broad ecosystem of related businesses, so we may also examine Whirlpool (WHR) and Pool Corp (POOL) as potential beneficiaries of a housing recovery. From there, broadening the lens to include homebuilders could help build a more complete, bottom‑up view of the housing sector’s dynamics.

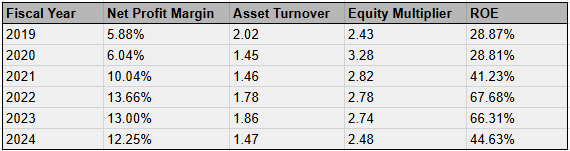

DuPont: operational ROE, not just leverage

Williams‑Sonoma is unusual among home retailers because it combines strong margins with solid asset productivity on top of a conservative balance sheet. Over the last several years, ROE has moved from the high‑20s into very elevated territory, driven by higher net margins, while financial leverage stepped up around 2020 and has since trended lower again. In other words, today’s ROE reflects healthier underlying profitability more than an aggressively debt‑heavy capital structure.

Most furniture and home retailers run asset turns around roughly 1–1.5x on a consolidated asset base, and Williams‑Sonoma sits in that band rather than enjoying some uniquely superior asset efficiency. Wayfair, by contrast, has typically posted asset turns in the 3x‑plus range, reflecting that an online‑only model can generate much more revenue per dollar of reported assets than store‑based peers.

Despite those very high turns, Wayfair has usually produced negative or very weak ROE because its net margins are structurally negative, which shows that high sales per dollar of assets are not enough without disciplined pricing and cost control. What really sets WSM apart is that it layers meaningfully higher net margins on top of fairly normal asset turns while keeping financial leverage only moderate, so its ROE is consistently better than peers primarily because it earns far more profit on each dollar of sales - not because it starves the business of assets or juices returns with excessive debt.

Brand ladder and product economics

Williams‑Sonoma’s margin structure starts with a deliberately engineered brand ladder that lets the company sell premium, mostly proprietary products to upper‑middle and affluent consumers across their entire life cycle. That architecture is what allows WSM to run gross margins in the mid‑40s, well above the furniture and fixtures industry average in the mid‑30s and comparable to only a handful of higher‑end peers. Recent disclosures show gross margins in the mid‑40s to high‑40s in many quarters, underscoring that this is not a one‑off pandemic artifact.

At the corporate level, WSM operates a family of brands: Williams Sonoma and Williams Sonoma Home, Pottery Barn, Pottery Barn Kids, PBteen, West Elm, Rejuvenation, Mark & Graham, GreenRow, and Dormify. These are not independent banners thrown together over time; they are arranged as a staircase that tracks household formation and rising income. Dormify, PBteen, and Pottery Barn Kids give WSM an entry point with younger consumers and young families - dorm rooms, teen bedrooms, children’s spaces. As those customers age into their first serious apartments, West Elm becomes the natural next stop: modern, design‑forward furniture and decor positioned above IKEA and Wayfair in quality and price, but still accessible for urban professionals.

When that same household moves into a larger home and starts thinking in terms of furnishing the house instead of buying one‑off pieces, Pottery Barn takes over as the classic, higher‑end family brand, skewing toward more traditional or transitional aesthetics and larger‑ticket, whole‑room projects. Above Pottery Barn sits Williams Sonoma Home, positioned as a higher‑end furniture and decor label with more formal looks, higher price points, and a target customer who might otherwise be shopping RH or designer showrooms. Rejuvenation operates as a specialist, architectural‑grade brand: heirloom‑quality lighting, hardware, and some furniture, much of it made‑to‑order in Portland and sold into high‑end renovations and professional design projects. The flagship Williams Sonoma brand wraps around all of this, selling premium kitchenware, electrics, and tabletop from blue‑chip third‑party names like All‑Clad, Le Creuset, and SMEG, plus proprietary lines.

The economic consequence is that WSM captures a much higher lifetime value per household. Cross‑brand customers already account for roughly 60% of sales, reflecting the ability to move buyers across the portfolio as their life stage and income change. A student who encounters Dormify can graduate into West Elm, then migrate into Pottery Barn when buying a home, and eventually furnish a second home or major renovation using Williams Sonoma Home and Rejuvenation. Because this happens within a single corporate family, WSM can reuse data, creative, and infrastructure across brands, making marketing spend far more efficient than mono‑brand competitors.

Underneath the banners, WSM has made a strategic decision to be a design‑led, mostly proprietary retailer. Management has highlighted that over 90% of products sold are proprietary, designed in‑house and made exclusively for the company’s brands, either in its own facilities or by a tightly managed supplier network. That exclusivity is central to the margin story. When a Pottery Barn sectional or West Elm dining table does not exist anywhere else, customers cannot run a clean price comparison on Amazon or at Ashley, which reduces direct price competition and lowers the need for chronic couponing. Being the design and volume owner also shifts bargaining power in the supply chain; vendors are more interchangeable when WSM controls the design, making it easier to negotiate favorable unit economics and preserve gross margin when input costs or tariffs move.

It also matters where these brands sit on the price spectrum. On many like‑for‑like items, West Elm and Pottery Barn are meaningfully more expensive than IKEA, Ashley, or Wayfair, but they do not push as far into the ultra‑luxury tier as RH. A West Elm or Pottery Barn sectional commonly falls into the low‑ to mid‑thousands, with materials and construction that justify the ticket for an upper‑middle‑income household, while mass‑market chains like Ashley often cluster in lower price bands with cheaper construction. RH frequently stretches to higher price points, tied to a very heavy, gallery‑centric real‑estate model and associated cost structure that raise capital intensity even when gross margins are also high.

WSM, particularly through Williams Sonoma Home and Rejuvenation, can reach into that aspirational and luxury customer segment without inheriting RH’s level of real‑estate intensity. As those higher‑end banners grow faster than the rest of the portfolio, the overall company mix naturally shifts toward richer categories and customers, creating a built‑in tailwind to profitability. Taken together, this brand strategy produces three reinforcing financial effects: ticket size and mix skew higher than mass peers; strong brands reduce the need for constant promotions; and multi‑brand lifetime monetization stretches customer economics over decades rather than single transactions.

Data, inventory, and margin discipline

Proprietary products insulate WSM from direct price comparison, as discussed. But the margin story does not stop there. By linking name, email, and physical address to roughly 70% of purchases across brands, WSM has built a data advantage over two decades that allows far more precise targeting than most competitors. Management and executives have emphasized that this cross‑brand database of tens of millions of households underpins personalized outreach and cross‑selling.

Most furniture retailers are trapped in a margin squeeze: they cannot reliably identify their best customers, cannot forecast demand accurately, and end up liquidating aged inventory at heavy markdowns. WSM’s system inverts this. When the company knows a West Elm buyer has just had a child, it can target them with Pottery Barn Kids at regular price rather than clearing inventory six months later. Higher conversion at full price versus chronically discounted inventory is a structural margin advantage.

The unified inventory system amplifies this. As EVP Patrick Connolly has described, when an item is out of stock online, WSM’s systems can surface nearby stores that have the item and route demand there, while overstocked store units can be effectively transferred into the online “warehouse” where they are more likely to sell without markdowns. Imagine a West Elm sofa that sells well online but stalls in a handful of stores: in a traditional chain, those stores would stack it on the clearance floor and start cutting price, but in WSM’s model that same sofa can be sold to an e‑commerce customer or another market that still wants it at full price. Coupled with increasingly sophisticated forecasting that trims how much speculative stock WSM buys in the first place, the result is less overstock, less forced discounting, and more margin protection at scale.

WSM’s durability is more than just brand strength. It reflects systematic, data‑driven pricing and inventory discipline that compounds with scale: the more customers WSM identifies, the more precisely it targets; the more it targets, the less it discounts; the less it discounts, the more it learns about true demand.

This explains why WSM largely avoids the perpetual promotional grind that characterizes much of furniture retailing. But understanding what WSM does with data is only half the story. The other half is how the company built the systems to collect, unify, and act on that data over decades.

How WSM built its omnichannel engine

The omnichannel story at Williams‑Sonoma is not a quick pivot from malls to mobile; it is the product of roughly three decades of incremental, compounding decisions that all pulled in the same direction. Understanding that arc makes it easier to see why the model is so hard to copy.

The roots go back to catalogs. Long before “direct‑to‑consumer” was a buzzword, Williams Sonoma and later Pottery Barn were running substantial catalog operations, shipping product off centralized inventory to customers whose names, addresses, and purchasing histories the company tracked closely. While most furniture retailers were building ever‑denser store fleets, WSM was learning to merchandise through photography, fulfill individual parcels from regional facilities, and market directly into the home. By the late 1990s it already behaved, operationally, like a mail‑order platform rather than a pure store chain.

When the web arrived, that legacy gave WSM what Scott Galloway later described as a “20‑year head start in omnichannel.” The first major digital initiative was not a broad e‑commerce rollout but the Williams Sonoma registry in 1998, which moved a high‑value, life‑event use case online and tied it to the existing catalog and store infrastructure. That move forced the company to solve for cross‑channel identity, order capture, and fulfillment far earlier than peers. By the early 2000s, WSM could see across store, catalog, and web transactions at the customer level in a way that today gets described as “unified commerce”.

Laura Alber grew up inside that direct business. Before becoming CEO in 2010, she had run Pottery Barn, including its catalog and online operations, and had a very clear view that the store had to become one touchpoint in a larger system, not the center of the universe. When she took the top job, she articulated: Williams‑Sonoma would be “digital first, but not digital only.” In practice that meant the company would plan assortments, marketing, and customer journeys from the perspective of a customer who starts online or on a phone, and only then think about what the store experience should add.

From that philosophy came a series of organizational and systems decisions that are incredibly hard for competitors to unwind. One of the most important was eliminating channel conflict. WSM reworked compensation so that store associates receive credit when they help customers place online orders, whether in store or later, instead of being punished when a sale “leaks” to the website. That one change means store staff are happy to pull up the site, order colors or sizes not on the floor, or send a client home with digital lookbooks rather than forcing a sub‑optimal in‑store close.

At the same time, the company invested heavily in unifying inventory across channels. Rather than segregating stock by store or catalog, it built systems that treat the entire network - regional distribution centers, brand‑specific distribution centers, and stores - as one pool. If the e‑commerce channel is out of a given SKU, the system can surface nearby stores that still have it and route an order there; if a store ends up long inventory in a style that is selling online, the product can be reallocated virtually and shipped to the consumer without a margin‑killing markdown. For a legacy retailer it required a decade of systems work and process change to approach the kind of routing that is taken for granted in digitally native businesses.

Rather than chasing square footage for its own sake, WSM built a smaller set of high‑productivity showrooms and regional distribution centers that feed every channel at once. Store openings and closures over the last decade reflect that mindset: pruning under‑productive locations, leaning into larger, experience‑driven formats where they make sense, and otherwise letting digital do the heavy lifting. In parallel, WSM opened and expanded large distribution centers, like its 1.25‑million‑square‑foot facility in Glendale, AZ, designed from the outset to serve multiple brands and geographies with high automation and direct‑to‑consumer shipping.

On top of that physical footprint, the company layered technology that tightens the machine. The 2017 acquisition of Outward, a 3‑D imaging and visualization company, was a way to reduce returns and increase conversion by letting customers see furniture in realistic context before buying. Better visualization means fewer costly “didn’t look like I expected” returns and a higher likelihood that customers commit to larger projects online. More recently, WSM has rolled out Salesforce’s Agentforce 360 across its brands to unify customer support data and bring AI into service interactions, a move that allows agents (in stores or contact centers) to see a full cross‑brand history and, over time, for algorithms to anticipate needs and nudge the right offer at the right time.

The pandemic stress‑tested all of this. In interviews, Alber has described modeling scenarios in early 2020 where revenue went to zero; instead, the opposite happened. As stores closed, associates immediately pivoted to serving customers by phone, chat, and video from their homes, while the unified fulfillment engine simply rerouted orders away from closed locations and through distribution centers or ship‑from‑store where possible. Because so much of the demand machinery was already digital and inventory was already pooled, WSM could absorb the shock and then ride the surge in home‑furnishing demand without the chaos that hit less prepared chains.

Today, roughly two‑thirds to seventy percent of WSM’s revenue flows through digital channels, but the important point is not the percentage, it is that the distinction between “store” and “online” is operationally thin. A customer might discover a sofa on Instagram, see it in a West Elm showroom, work with a designer in Pottery Barn to pull together a room, and ultimately check out through a mobile app; the same back‑end decides how to fulfill, where to source, and what follow‑up offers to send. For investors, what matters is that decades of work on this engine let WSM push more revenue through a relatively lean asset base, with fewer frictions and less waste, which shows up in its unusually strong margins.

What I want on a buy list

What I’m really trying to build with a personal buy list is a small set of businesses I think are the best in their lane and likely to emerge stronger from the next rough patch, not just survive it. Williams‑Sonoma fits that mold for me. On the surface it’s a furniture retailer; underneath, it’s a mix of proprietary design, a carefully stacked brand ladder, years of customer data, and an omnichannel setup most of the industry is still chasing.

That combination, high returns on capital, sensible balance sheet, and a model that should gain share when weaker players stumble, is exactly what I want to have pre‑underwritten before volatility shows up.

Disclaimer

This article is educational analysis based on public filings, historical records, and industry data. It represents the author’s interpretation of available information and is not investment advice. Nothing in this article should be construed as a recommendation to buy, sell, or hold any security or financial instrument. Past performance and historical patterns do not guarantee future results. The author may hold positions in companies discussed. Readers should conduct their own independent research and consult with qualified financial advisors before making any investment decisions. All statements about future developments, regulatory changes, or market disruptions are speculative and subject to substantial uncertainty.

Thanks for bringing this company to our attention, very well articulated.

Amazing company, but too expensive..